The Chart of Accounts (COA): Why Getting It Right Matters More Than You Think

If you’ve ever tried to pull a financial report and ended up with numbers that just didn’t make sense? Revenue in the wrong category, expenses that seem to appear from nowhere or totals that don’t tell you anything useful. It’s possible the problem started long before anyone ran that report.

It might very well have started with the chart of accounts.

Many small and midsize business owners don’t give the chart of accounts nearly the attention it deserves. It’s often set up quickly at the beginning, left untouched for years and rarely thought about again … until something goes wrong.

Getting it right from the start, and maintaining it well over time, is one of the most impactful things you can do for the financial health of your business.

What Is a Chart of Accounts?

A chart of accounts (COA) is a structured list of every financial account your business uses to record transactions, typically broken down into assets, liabilities, equity, revenue and expenses.

It’s effectively the backbone of your company’s accounting. Every time money comes in or goes out, every time an asset is acquired or a liability is incurred, that transaction gets assigned to one of the accounts in your COA.

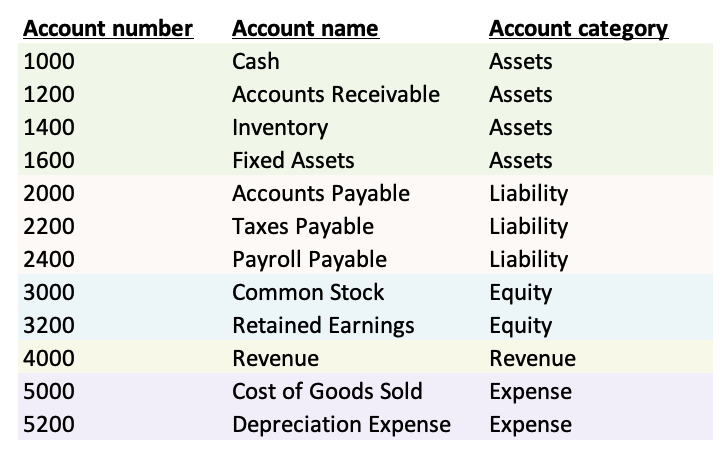

This is an extremely basic example that uses some common categories just to give you an idea of what one might look like:

McManamon & Co.

Your chart of accounts might include additional columns such as the financial statement the account belongs to, sub-categories, even descriptions depending on how many people might need to access the COA.

When your chat of accounts is well-organized, your financial reports should be more accurate, meaningful and easy to use. When it’s not, the ripple effects can touch everything from your monthly profit-and-loss statement to your tax filing.

Common Mistakes Businesses Make

Many businesses stumble when setting up or managing their chart of accounts. Some of the most frequent missteps include:

- Starting with a generic template and never customizing it. Most accounting software comes with a default COA, which is a fine starting point. However, a landscaping company’s financial environment might look very different from a software firm. A COA that isn’t tailored to your industry and business model could create ambiguity from the get-go.

- Creating too many accounts (or too few). More accounts don’t necessarily translate to more clarity. If every minor expense gets its own line item, reports could become cluttered and difficult to interpret. On the other hand, lumping everything into broad categories like “miscellaneous expenses” might make it almost impossible to identify where the business’s money is actually going. Your goal should be a structure that’s detailed enough to be informative but streamlined enough to be manageable.

- Inconsistent naming conventions. Not everyone is laser-focused on consistency. If accounts are named differently by different people, or even by the same person at different times, it can create confusion and make reporting unreliable. If travel expenses are sometimes coded to “Travel,” but sometimes to “Travel & Entertainment,” and other times to “Business Travel” … well, how do you expect to get an accurate picture of that spending?

- Failing to use account numbers strategically. A logical, numbered account structure helps organize your COA and makes it easier to expand over time. Without a consistent numbering system, the process of adding new accounts over time could leave your COA messier and more disorganized.

- Not revisiting the COA as the business evolves. Much like a landscaping company and a software firm might have different COA needs, a chart of accounts that worked perfectly for a two-person startup might be inadequate for a 30-person company with multiple revenue streams. Businesses change; the COA sometimes has to change with them.

How a Poorly Organized COA Leads to Bad Data

The consequences of a disorganized chart of accounts aren’t just cosmetic. They’re operational and strategic.

When transactions are coded to the wrong accounts — either because the accounts aren’t specific enough, or because the structure is confusing — your financial statements start reflecting fiction rather than reality. Profit margins look different than they actually are. Certain expenses appear inflated while others seem nonexistent. Budget variances become impossible to track or explain.

This bad data then flows downstream into every decision that relies on your financial info. Are you pricing your products or services correctly? Should you hire? Can you afford that equipment purchase? If your COA is feeding inaccurate data into your reports, the answers you’re getting to those questions may be leading you in the wrong direction.

There are tax implications, too. Misclassified expenses can mean missed deductions or incorrectly claimed deductions, creating audit risk. A well-structured COA helps ensure that tax-relevant transactions are captured accurately and consistently throughout the year.

Tips for Building a COA That Grows With Your Business

A strong chart of accounts doesn’t have to be complicated. Here’s some advice for putting together your COA:

- Align your COA with your business model. Thinking about how your business actually operates. What are your key revenue streams? What are your major cost drivers? How do you want to measure performance? Let those answers guide your structure.

- Use a logical numbering system. Look back at the graphic above. That’s a typical numbering system, with asset accounts starting with 1, liabilities with 2, equity with 3, revenue with 4 and expenses with 5 or higher. This makes it easy to navigate and leaves room to add accounts within each category.

- Build in room to grow. Leave gaps in your numbering so you can insert new accounts in the right places without disrupting the overall structure. Planning for growth is much easier than trying to retrofit it later.

- Establish clear naming conventions and stick to them. Document your naming rules and make sure everyone involved in bookkeeping follows them consistently.

- Review your COA at least annually. Again, business needs evolve. A periodic review helps you identify accounts that are no longer relevant, categories that need to be broken out further or new areas that need to be added.

- Work with an accounting professional. Especially when setting up a new business or going through a significant transition, having an experienced accountant help structure your COA can save considerable time and prevent costly errors down the road.

How McManamon & Co. Can Help

A well-built chart of accounts is the foundation that makes everything else in your financial reporting work the way it should. Whether you’re starting from scratch, cleaning up an existing structure or managing a growing business with increasingly complex financials, getting your COA right is worth the investment.

McManamon & Co. is an accounting, tax, fraud, forensic and consulting firm that serves small and midsize businesses across Northern Ohio and South Carolina. Our experienced accounting team can work closely with you to create your COA, financial statements and more, as well as train your own accounting staff in software programs and best practices.

Call us at 440.892.8900 or contact us online today to learn how we can help you get your financial foundation right.

Tags: accounting, McManamon | Posted in accounting, McManamon & Co.